What can a financial adviser do for me?

You might be saying to yourself;

• I don’t have enough money or assets to get financial advice, or

• I don’t have enough time to see a financial adviser, or

• Is it worth getting financial advice, or

• What exactly does a financial adviser do?

These are all reasonable objections an adviser would experience from roughly 60% of those Australians who don’t already have a financial adviser. Even those people who have had a financial adviser for many years might only have sought advice on one subject such as life insurance and may not know the extent of the services that their financial adviser can provide them.

Why is this the case?

Let’s look at a couple of the objections why people don’t seek financial advice.

“I don’t have enough money to see a Financial Adviser”

A common reason most Australians don’t seek financial advice is because they believe they don’t have enough money or assets in order to justify seeking financial advice.

While its true that a financial adviser helps some people who would be considered wealthy become even wealthier. The bigger truth is that the majority of clients the average adviser has (that’s me) is made up of everyday Australian’s with ordinary jobs earning average incomes… sound like you?

What I am trying to say here is that you don’t need to already be wealthy to seek financial advice. In fact there is a good chance that you will derive a greater benefit from financial advice if you are not already rich.

You are more likely to become wealthy, and more importantly stay wealthy with help from a financial adviser, rather than going it alone.

One of the best attributes of a good financial adviser is they “stop clients making silly mistakes” i.e. stopping clients towards the end of the GFC from moving their money out of their current investment option into a more conservative option. When asked why, most responses were because they didn’t want to lose anymore super…if you don’t know why this could have been a costly mistake then you certainly needed to seek the advice of a financial adviser.

“I don’t have the time to see a Financial Adviser”

A second reason for not seeking financial advice is the “I don’t have time” excuse.

We will always find time for something we think is important, so the real reason for many people not seeking advice is not lack of time, it’s that they don’t think planning for their future is important enough.

Let’s face it what’s more important?

• finding enough time to catch up with a mate for a beer or a best friend for coffee or

• Spending the same amount of time discussing your financial future?

Be like myself and the majority of my clients find time to do both as they are both important.

Or even better, make an appointment to discuss your financial future with me and I’ll have that coffee with you!

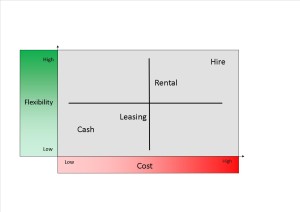

The flexibility of these options along with the net cost to the business is something that should not be over looked. Lease and chattel mortgages can tie businesses down for long term periods and reduce flexibility. On the other hand, equipment hire is very expensive and may leave you open to availability and weather issues. Consider the adjoining chart.

The flexibility of these options along with the net cost to the business is something that should not be over looked. Lease and chattel mortgages can tie businesses down for long term periods and reduce flexibility. On the other hand, equipment hire is very expensive and may leave you open to availability and weather issues. Consider the adjoining chart.