Financing your asset purchases

For most businesses, the decision for financing your asset purchases is very clear cut as it boils down to a choice between a lease or a chattel mortgage. There are, however many businesses who may find a short term rental contract the best option available. For businesses that may not qualify for traditional bank lending or have specific needs, short term rental finance can offer many benefits, please consider the following list:-

- Start up equipment finance when banks don’t want to know you

- No capital outlay, keep your cash for more important things

- 100% tax deductible monthly payments

- Fast approval – 24 – 48 hrs / easy application

- No financials under $50,000*

- Maxed out capital expenditure budget

- Choices available at the end of the 1 year term

Once the rental term is over, the business has 4 choices:-

- Hand the equipment back as it has served its purpose

- Continue to rent

- Buy the equipment outright and get a 75% rebate on all the rental repayments made

- Switch to a ‘rent-to-own’ plan for another 3 years where the equipment is owned at the end of the term

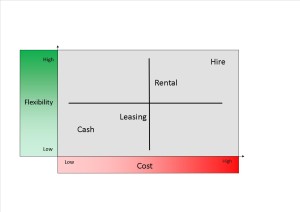

The flexibility of these options along with the net cost to the business is something that should not be over looked. Lease and chattel mortgages can tie businesses down for long term periods and reduce flexibility. On the other hand, equipment hire is very expensive and may leave you open to availability and weather issues. Consider the adjoining chart.

The flexibility of these options along with the net cost to the business is something that should not be over looked. Lease and chattel mortgages can tie businesses down for long term periods and reduce flexibility. On the other hand, equipment hire is very expensive and may leave you open to availability and weather issues. Consider the adjoining chart.

The rental option is a pathway to ownership while at the same time presenting you with a very economic alternative to bank finance, particularly if your business fits into one of the categories highlighted above.

For example, a $30,000 service van for your business would rent for $355 per week, after 12 months the buy back price on this asset would be $20,036. Lets consider each of the end of term options mentioned above:-

- Hand the equipment back as it has served its purpose – The total rent paid would be $18,495 and the tax deduction claimed on these rental payments for a company would be approximately $5,550 (30% tax rate). The net payments would total $12,946, therefore by adding the end of year 1 purchase price to the net payments the rental cost of ownership would be $2,157 or $41.50 per week against having purchased the van outright. The revenue and profit generated by the asset should be well above this cost.

- Continue to rent – If your contract ran for a few more months, you could still exercise the above option at the completion and each rental payment would continue to add to your rebate total if you decided to purchase the asset.

- Buy the equipment outright and get a 75% rebate (net of tax) on all the rental repayments made – Net of tax requires the deduction of 10% input tax credits claimed from the 12 month rental figure before multiplying the total by 75%. This is then subtracted from the purchase price and tax is added back on for sale back to your business at a price of $20,036.

- Switch to a ‘rent-to-own’ plan for another 3 years where the equipment is owned at the end of the term – rental payments are reduced by approximately 30 % during this period.

*Each application is assessed on its own merits

For more information on financing your asset purchases, please contact Chris at TWM Finance on 07 3281 1226.

Leave a Reply

Want to join the discussion?Feel free to contribute!