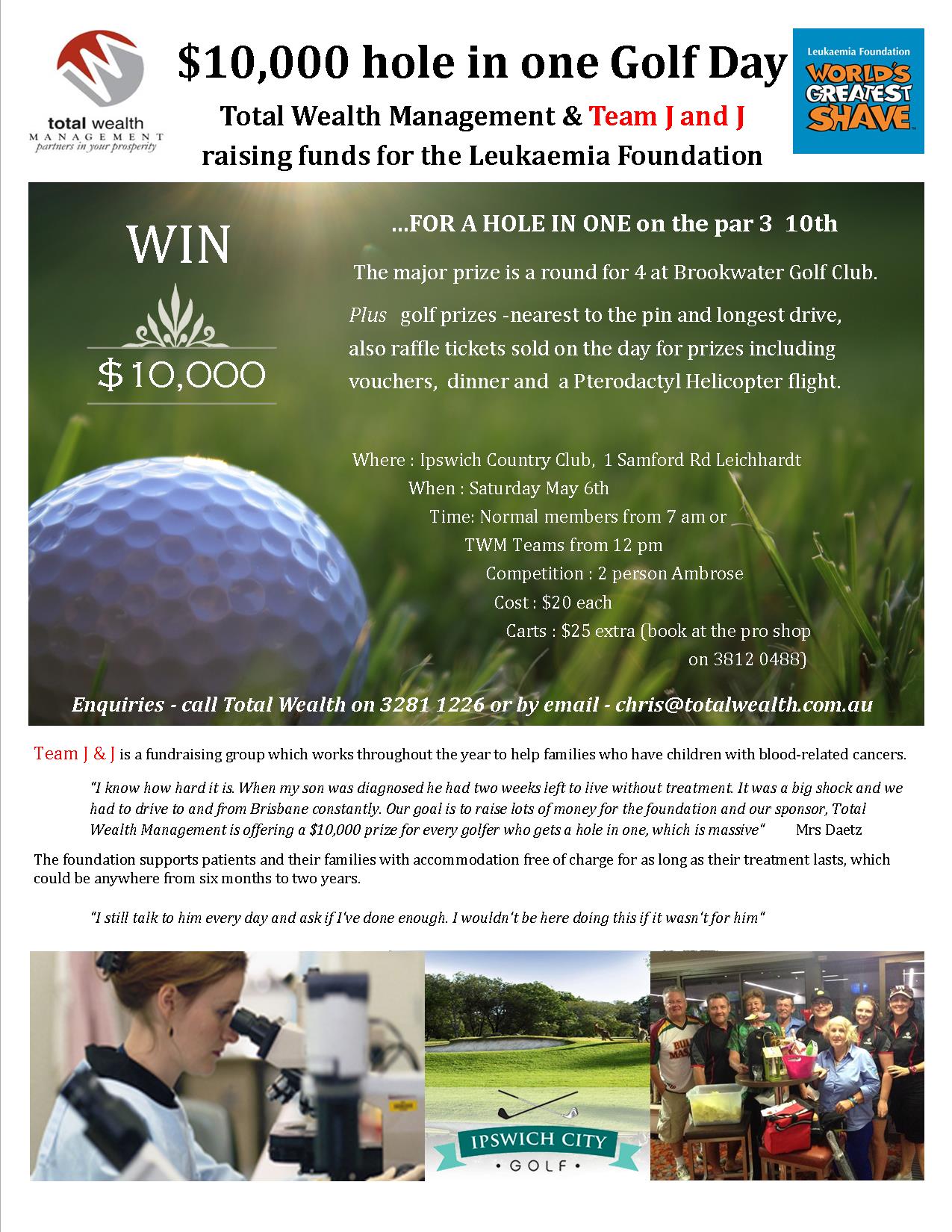

The Total Wealth Management $10,000 hole in one tournament supporting Team J & J to raise funds for the Leukaemia Foundation has been ‘run and won’.

Unfortunately no one aced the par 3, 10th hole with the nearest shot from Ian McNabb who was only 4’ away. Ian won a dinner for two donated by Sirromet Wines. Our winners were Martin Manning and Troy McGuinness with a net 60; they won a round for 4 at Brookwater Golf Club as well as the usual member’s prize. The best score from one of the TWM teams was from John King and Steve Lampard who handed in a net 64. A strange coincidence occurred when one of the nearest to the pin prizes of a bottle of red wine that I personally donated was handed straight back to me when I won the prize for that hole. Oh well, I guess I’ll just have to donate it again next year.

The atmosphere on the 10th tee was fantastic as each player from the field of 169 attempted to pick up the cash prize. A big thank you to Narelle, Anne, Monica and Emma for supervising the hole in one attempts on the day and for some fun interaction with the players.

I can announce that a total of $3,200 was raised thanks to the tireless work of Gayle, Kate and Robert on the day and over the weeks leading up to the event. We all look forward to another successful day next year so mark your calendar for 2018 and the 1st weekend in May.

AMP have put together a great article where they have asked a number of leading investment advisers what advice they would give to their 20 year old self. Well worth a read. Please click on this link, Investing

If you have any questions please give our office a call, having a mentor to help you move forward through the financial markets is very important and that is what we specialise in. It costs nothing to ask and little effort to organise an appointment. It may well be the best decision you ever make.

How following the strategies of a tennis champion

can make you Wealthy

How did Roger Federer win the Australian Open and what does he have to do with wealth creation? He’s 35, had knee surgery 12 months ago, was ranked 17th and had to play 3 top ten players, just to get to the Final.

How about, Roger knows how to take care of business. He doesn’t wait until the second Set to win. He starts from the get-go.

Let’s look at some stats;

• Roger Federer won the first set of Every Match he played in the Australian Open.

• For the first three sets of every match, he won either two or three of the sets.

• Out of Seven games, he only played three five setters.

Basically, he doesn’t wait to win. He gets on with the job from the first serve. Sure he has some resistance from better players, especially in finals. But by winning the first set he sets the tone of the match, he controls the game. By moving early, Roger Federer gets the advantage.

Physically he is at an advantage because he doesn’t have to work as hard as he is playing less sets over the course of two weeks. At 35, each set adds up – especially come the Final.

Psychologically, he forces his opponents into a defensive position, where they have to adjust their strategy to compete with him. He is able to maintain composure throughout the Match, as he is always in front.

So how does this translate to being wealthy? Well, unless you’re a tennis pro this exact strategy probably doesn’t translate directly. But if you’re an average punter, there is an important lesson here.

Start Early.

Get ahead sooner rather than later. Don’t wait for the right time. Just do it. Wealth creation is a long term project.

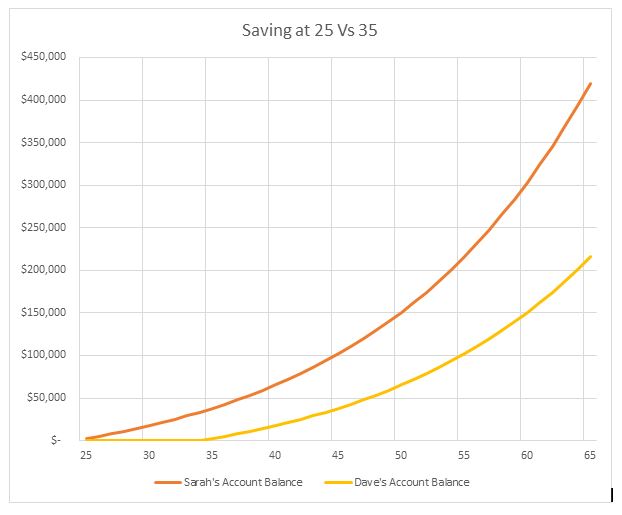

Let’s look at a financial example. Sarah and Dave contribute $2,400 pa into an investment. The only exception is that Dave is going to start 10 years later. Now obviously, he is going to have a smaller balance at age 65 when they both retire, but how much is the scary part.

Just do it!

Sarah gets to retirement with a whopping $419,000, whereas as Dave only has $215,000.

That means $204,000 is the cost of delay!

Even crazier, the end balance for Sarah is generating $23,000 pa, compared to Dave who is pulling in just $12,000 pa. Sarah will get paid twice as much for her wealth creation in retirement as Dave will, just because she started ten years earlier.

Two key takeouts from our lessons in tennis.

One -If you want to be the local tennis pro – finish your games early (in time for a quick beer or maybe a round of golf in the afternoon) and give up the five setters (your knees will thank you for it).

Two – if you want to make money through investing, start early. Delaying a wealth creation plan will only cost you.

We often come across people who know they should be thinking about the future, but are caught up in day-to-day life and not planning for retirement. They cannot see beyond the present and into the future and as such find it hard to comprehend what the future may hold.

Have you ever wondered why it is easier to buy a car than it is to save for retirement?

We know that the second a car rolls off the lot it significantly reduces in value. Compared to that your super is likely to actually increase in value over the life of the vehicle. Why then do people find it easier to buy a car?

Because of immediate gratification – we get something straight away.

After you’ve signed the paperwork and handed over a huge amount of cash, you get to enjoy your Brand New Shiny Car – all for you.

Sure your money is gone, but look at the car…

How do you feel about your shiny new car a month later? Or a year later?

You probably have gotten to the point of washing it once a month (yes, driving through a thunderstorm counts as cleaning), letting the kids eat in the back and you don’t mind if someone gets a bit of dirt on the upholstery. By this time the new car obsession is gone.

You see buying a car might provide satisfaction in the here and now, but it rarely holds value (in our minds and in the marketplace) for more than a year and is it really the best place for your money?

Planning for retirement

Planning for retirement on the other hand doesn’t usually give you immediate gratification, but it is a prudent place to invest.

We think that if we save a little more and add it to our super we’ll be right when we get to retirement age. But that’s the problem, we think we’ll be alright, but we don’t know.

With a new car purchase, we know exactly what we are getting and receive our car as soon as we hand over some cash. We have certainty. But with retirement (being so far into the future) we have no idea what our retirement will look like.

So, how do you get the best of both worlds – gratification and certainty?

We approach this by showing you your future financial position using your current situation and alternatives. We make it possible to see what your retirement looks like, 10, 20, 30 years down the track. We do this so that when you make a contribution to your super fund or decide to purchase an investment property, you know that this will ensure you can enjoy a comfortable retirement.

This regular review process allows for us to provide greater certainty to you and hopefully greater peace of mind. It allows for you to draw the connection between depositing funds to super and the benefit you will receive (albeit in the long term future).

Most importantly though, planning for retirement provides a sense of gratification today for making progress towards your long term future prosperity.

We speak to a lot of people about insurance and they often don’t understand the difference between health insurance, income protection and trauma insurance.

One of the biggest reasons people often get confused is that while all of these insurances relate to a person’s health, they have a wide range of benefits which are often perceived as being similar, when in fact they are very different.

Health Insurance

Health insurance provides a range of benefits, based on the level of cover you have. One of the biggest reasons for choosing health insurance is to avoid paying the Medicare Levy.

Health insurance provides a range of benefits, based on the level of cover you have. One of the biggest reasons for choosing health insurance is to avoid paying the Medicare Levy.

If you have a Comprehensive level of Health Insurance you may have an Extras package, which will provide you with additional benefits such as dental, optical, chiropractic.

Generally, the level of cover you hold determines a gap amount or a rebate amount. For example, you may receive a 55% rebate on regular dental check-ups. This rebate usually comes with an annual rebate amount – i.e you may be limited to claiming up to $500 pa on dental.

Effectively, Health Insurance relates to the expenses of health care.

Income Protection

Where Health insurance covers health care expenses, Income Protection covers your lost salary if you are sick or ill.

In fact, Income Protection simply provides you with a monthly cash amount, based on the level of cover you have taken out. So, if you are unable to work, because you are sick or ill, you will be paid the monthly benefit until you can return to work.

There is no mandate that states what you must spend your income protection benefit on. It could be medical expenses, it could be on food or the mortgage – it is entirely up to you.

Trauma

Similarly, to income protection, trauma is a cash payment, that can be used for anything you wish. However, trauma is a lump sum payment that is generally reserved for critical illnesses, such as cancer, heart attack and stroke.

Trauma insurance works in conjunction with Health insurance to ensure you are not left out of pocket, when you are diagnosed with a major illness. While Health insurance may cover a lot of medical expenses, there are often limits or gaps, that can mean you are still required to pay for medical costs – not something you want to worry about when deciding to get lifesaving surgery!

Why should I have these insurances, if they are so similar?

While each of the insurances do have similar circumstances under which to claim, the benefits provided by each of these insurances varies widely;

Rather than thinking of these as the same thing, it is best to think about them as complimentary policies that provide a total insurance health plan.

In this 3-part blog series on financial advice, we look at the why it is hard to differentiate value between financial advisers, the limitations of company aligned advisers and whether you should go direct or not. This is part 1 of the series.

For most people, it can be hard to identify the different value between financial products and services.

I think most of us find it difficult because most daily purchase decisions involve products (TV, home/ contents insurance, health insurance, new car, new home etc). In these situations, we make our decision based on brand, cost, online reviews, reading the product brochures and possibly doing some research. We take all these things into account and make a decision to purchase that product. Financial advice from an adviser is no different.

Purchasing a financial advice service or product on the other hand can be far more difficult to evaluate, mainly because you often don’t have a physical product to look at or the benefits and services being provided may not provide an immediate benefit, and in fact may cost even more money.

Life Insurance is a good example of this. We apply now, start paying premiums for a product we don’t get to use now and in our mind (remember we don’t think anything will happen to us until we are old) we won’t get a benefit for years, and maybe never if we don’t make a claim.

Life Insurance is a good example of this. We apply now, start paying premiums for a product we don’t get to use now and in our mind (remember we don’t think anything will happen to us until we are old) we won’t get a benefit for years, and maybe never if we don’t make a claim.

For many of us we find it difficult to put a value on peace of mind, which is what insurance offers.

The same difficulty occurs when picking picking financial advice from a financial adviser. How do you evaluate the effectiveness of the service delivered to you by a financial adviser, today? You might have a good idea in 5 or 10 years’ time whether the advice was right for you – but how do you know today?

Yes, an adviser can find a cheaper insurance premium, get a better interest rate or save some tax – but what about long term planning, like ensuring you have sufficient super to pay for your retirement – you won’t know until you retire.

Because great advice can be hard to identify, people often choose an adviser, or a financial services product, based on the short-term information of price. The rationale is that without knowing why one should pay more for a particular financial adviser, many will opt for the cheapest – but this can be dangerous.

Lower priced planners generally have limitations of on the types of advice they can offer or the brand of products they can recommend. They may have to sell a particular number of financial products to meet sales quotas or they may have a vested interest in ensuring you do not move your money from the administration of their employer.

This means that while you are getting financial advice, you are not getting the financial advice that is right for you, individually.

In the following post we look at the limitations of company aligned advisers and how this can impact the financial advice you receive.

11 Lawrence St, North Ipswich QLD 4305

Contact Us

Phone: (07) 3281 1226Postal address

PO Box 2648, North Ipswich QLD 4305