A challenging year for investors, with rising uncertainty

Markets began the year with considerable optimism. The global economy was performing well, underpinned by strong growth in the US and China and evidence of recovery in Europe and Japan, while President Trump’s corporate and personal tax cut reforms helped drive US corporate earnings and market momentum. For much of the year, investors downplayed risks such as rising interest rates, ‘quantitative tightening’ in the US and withdrawal of monetary stimulus in Europe, escalating trade tensions and elevated valuations in markets.

However, this complacent attitude ended abruptly in the final quarter. Markets became alarmed about the impact of further US interest rate rises, mixed news on the global economy (notably on Chinese growth), the potential failure of the trade truce between the US and China and rising political risk. Severe market volatility resulted in the worst year for share market returns since 2008. The new year begins with considerable uncertainty about the investment outlook.

Despite this, Table 1 shows that longer-term returns across a range of asset classes are still pleasing.

Table 1: Mainstream asset class returns in Australian dollars – periods to 31 December 2018

| Asset class |

Returns* 1 yr |

Returns* 3 yrs (pa) |

Returns* 5 yrs (pa) |

Returns* 10 yrs (pa) |

| Cash |

1.9% |

1.9% |

2.2% |

3.1% |

| Australian bonds |

4.5% |

3.7% |

4.7% |

5.2% |

| Global bonds (hedged) |

1.6% |

3.5% |

4.8% |

6.4% |

| Australian property securities |

3.3% |

7.6% |

12.5% |

10.7% |

| Global property securities (hedged) |

-3.0% |

4.2% |

8.0% |

12.6% |

| Australian shares |

-2.8% |

6.7% |

5.6% |

9.0% |

| Global shares (hedged) |

-7.4% |

7.6% |

7.5% |

12.3% |

| Global shares (unhedged) |

1.2% |

8.4% |

10.0% |

9.9% |

| Emerging markets (unhedged) |

-4.7% |

10.9% |

7.0% |

8.3% |

Benchmark data: Bloomberg AusBond Bank Bill Index (cash), Bloomberg AusBond Composite 0+ Yr Index (Aust bonds), Bloomberg Barclays Global Aggregate Index Hedged to $A (global bonds), S&P/ASX200 A-REIT Total Return Index (Australian property securities), FTSE EPRA/NAREIT Developed Index (net) hedged to $A (global property securities), S&P/ASX200 Total Return Index (Aust shares), MSCI All Country World Indices hedged and unhedged (net) in $A (global shares), and MSCI Emerging Markets (net, unhedged)

* Annualised returns. Past performance is not a reliable indicator of future performance.

Sources: FactSet, NAB Asset Management Services Limited.

Global growth moderated as the year progressed

While conditions in the global economy were generally favourable for much of the year, the outlook for 2019 is less certain as signs of slower growth in Europe and Asia emerged towards the end of 2018. Unlike the beginning of 2018, when growth was synchronised across the globe, 2019 begins with marked differences between regions and countries.

The US

The US economy enjoyed another year of strong growth, with economic indicators at the end of the year as positive as they were at the beginning. 2018 started well as a result of President Trump’s company and income tax cuts and substantial government stimulus. US corporate profit growth reached 25% annualised growth in the third quarter of 2018. An obvious sign of the economy’s strength was the progressive fall in the unemployment rate to 3.7%, which is near a fifty-year low. The tight labour market has given American workers more bargaining power, with the November US payroll report indicating average hourly wages grew 3.1%, the largest gain in nearly ten years. Wages growth, good job creation and enhanced job security helped underpin consumer sentiment and growth in retail sales.

The US Federal Reserve (the Fed) responded to these buoyant conditions by continuing to raise interest rates to keep inflation in check. The Fed increased the target federal funds rate by 0.25% four times during the year, to close at 2.25%−2.5%. In December, the Fed signalled the pace of rate increases would be more gradual in 2019. The Fed also maintained its ‘quantitative tightening’, selling US$50 billion of securities each month to reduce the US$4.5 trillion of US bonds and mortgage backed securities it had built up on its balance sheet since the GFC. This is a significant withdrawal of liquidity from markets.

Europe

After an encouraging start, economic conditions in Europe softened as 2018 progressed. The growth slowdown was broadly based, with Germany’s export-oriented economy particularly affected. Germany’s economy contracted by 0.2% in the third quarter, the first negative quarter in over three years. The growth of other economies also slowed. Economic concerns intensified later in the year due to the fragile state of the Italian economy, which is burdened by excessive debt, high unemployment and a weak banking system. After months of uncertainty, Italy’s populist coalition government reached agreement with the European Commission over proposed budget stimulus measures. Still, Italy’s economic and financial status remains precarious and could be an enduring source of concern for markets in 2019.

Europe’s slowdown is troubling markets because interest rates are already at very low levels. This means the European Central Bank (ECB), and policy makers generally, have limited ability to launch stimulus measures, if they become necessary. Despite this, the ECB concluded its quantitative easing program in December as planned.

The United Kingdom

In the UK, there were intense negotiations to reach a Brexit arrangement acceptable to both the UK and the European Union. However, 2018 closed with diminishing hope that an orderly withdrawal will be possible. A withdrawal agreement negotiated late in the year between Prime Minister Theresa May and the European Union was to have been ratified by the UK Parliament in December but the vote was deferred until January 2019 because there was little chance it would pass. If the re-scheduled vote fails, there is a real chance that an agreed Brexit withdrawal may not be in place on 29 March, the exit date. The uncertainty created by Brexit and consequent political instability has taken its toll on parts of the economy and affected the UK’s financial markets more than it has impacted global markets (so far). For example, business investment weakened in each of the first three quarters of 2018, and the Bank of England increased its policy rate in August as the pound’s depreciation led to inflation rising above its 2% target.

Japan

Despite years of substantial monetary stimulus and good growth in exports, Japan’s economy slowed and continues to lag the growth of other economies. Prices remain subdued, with inflation running near 1%. Although Japan’s unemployment rate is lower than America’s, there has been minimal growth in wages. This has contributed to slow domestic consumption growth. With interest rates close to zero, the Bank of Japan has little ammunition if the economy weakens further.

China

While it’s never easy to make a conclusive assessment of economic conditions in China, economic indicators suggest that growth moderated over the year. This was partly due to policy action by the central bank to underpin China’s financial stability by curbing credit growth. However, since mid-2018, Chinese authorities have implemented some targeted fiscal and monetary initiatives to support growth and lessen the impact of US tariffs. The trade dispute with the US has initially been unexpectedly beneficial to China’s trade performance, with exports to the US increasing 13% in the ten months to October compared with the same period in 2017. However, this was due to US importers bringing forward orders to escape new or higher tariff rates. This raises concerns for Chinese exports in 2019, especially if the trade ceasefire ends and the US resumes its program of tariff protection.

Trade tensions worsened through the year

Friction over trade escalated as the year wore on. Threats made by President Trump a year ago to impose tariffs to address America’s substantial trade deficit became a reality in 2018. After announcing in March that imports of steel and aluminium would attract a 25% tariff, in June the Trump administration imposed tariffs on Chinese imports totalling US$50 billion. China responded in the same way, targeting a range of US imports including aircraft, vehicles and agricultural products. In September, President Trump ordered the imposition of a 10% tariff on a further US$200 billion of imports from China.

A welcome attempt to reduce simmering trade tensions between the two economic superpowers occurred at December’s G20 summit. President Trump and China’s President Jingping agreed to reopen trade discussions and delay further tariff changes for 90 days, beginning on 1 January 2019. However, markets remain sceptical that a permanent reconciliation is possible because there remain significant differences between the two over issues such as intellectual property theft and cyber security. There are also lingering concerns that the Trump administration’s tariff policy could be extended to European car exports.

Volatility in the final quarter meant a disappointing year for global share investors

Share markets began the year with positive sentiment due to favourable global economic conditions and growth in corporate earnings, especially those in the US following company tax cuts. However, markets were rattled in the March quarter by higher than expected US wages data, which led to concerns the Fed may need to raise US interest rates more aggressively to keep inflation in check. The Trump administration’s decision to proceed with threatened tariff measures, targeting a range of products and Chinese imports in particular, also unsettled markets.

This uncertainty and market weakness proved short lived. Share markets in developed countries resumed their upward trend after March, although the length and breadth of the recovery was by no means consistent. The US enjoyed the most prolonged upswing, with buoyant economic conditions in the US and strong growth in company earnings pushing the market to its peak in September, when Japan’s Nikkei index also reached its high point for the year. By contrast, the recovery in European markets faltered by May due to global trade concerns, uncertainty created by the Italian budget impasse, the parlous state of the Italian economy and emerging signs that Europe’s economy had passed its peak.

Market sentiment worsened in the December quarter, resulting in considerable volatility in markets. Some severe falls pushed the returns of many markets into negative figures for the year. Global shares returned -7.4% for the year on an Australian dollar hedged basis, while the higher 1.2% unhedged return largely reflected the 10% fall of the Australian dollar against the US dollar. Following its 13.7% fall in the December quarter, the US S&P500 index returned -4.9% (in local currency terms) in the year, while Japan’s Nikkei index was down by 10.3%. In Europe, markets in Germany and France were down by 18.3% and 8.0% respectively. Elsewhere in Asia, Hong Kong’s Hang Seng index was down by 13.6% and China’s SSE composite index fell 24.6%.

The emerging markets sector endured a challenging year due to higher US interest rates, the strong US dollar and tightening global liquidity. Many investors chose to reduce riskier exposures such as emerging markets, particularly those in Latin America and Eastern Europe. Worst affected were emerging countries that are dependent on foreign capital, as higher US interest rates led to an outflow of capital from their economies back to the US. The higher US dollar has also exacerbated difficulties for those countries with borrowings denominated in US dollars. At the more severe end of the scale, Turkey and Argentina are experiencing economic downturns and very high inflation.

Our share market also lost ground, but outdid most major markets

Australian shares returned -2.8% in 2018, a markedly different result from the 11.8% return in the 2017 calendar year. In contrast to recent years, our market outperformed many of its developed global peers.

Performance varied across industry sectors. The Health Care sector was the strongest and most consistent outperformer for much of the year, rising 19.3% due to the superior earnings performance of a number of companies like CSL Limited. Information Technology (up 7.3%) was another strong performer, though it is a very small part of the Australian market.

However, the Telecommunications Services sector fell 17.9% as intense competition adversely impacted company profits, with Telstra forced to cut its dividend. Numerous headwinds adversely impacted the Financials ex-Real Estate Investment Trusts sector, which fell by 9.7%. The Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry was clearly a negative influence due to the adverse evidence it revealed. The market remains wary of possible recommendations by the Royal Commission that may result in substantial remediation, compliance costs and tighter lending standards. These increased costs will affect the profitability of financial institutions.

The Energy sector fell 21.3% in the December quarter and 8.6% over the year as slower global growth and elevated supply caused the Brent crude oil price to fall 19.6% during the calendar year. The Utilities sector fell 5.1%. Aside from the weaker oil price, utilities companies in the sector have become a political target, with calls for greater regulation to reduce the cost of power for Australian households.

Another mixed report card for Australia’s economy

Domestic economic conditions improved further in 2018, though economic statistics were more robust in the first half of the year than the second. By mid year, economic growth had picked up to 3.4% for the year, its fastest annual rate since 2012. However, Australia’s gross domestic product grew only 0.3% in the September quarter compared with 0.9% the previous quarter, which reduced the annual growth rate to 2.8%.

One positive feature of the year was the continued improvement in Australia’s labour market, raising hopes that wages growth may finally improve. After starting the year at 5.5%, strong jobs growth saw Australia’s unemployment rate fall to 5.1% at 30 November, the lowest in six years. The unemployment rate is close to the estimate of the Reserve Bank of Australia (RBA) of full employment (5%). This suggests spare capacity in the labour market has diminished to the point where wages growth should start to recover. Encouragingly, wages growth picked up to a 2.3% annual pace for the September quarter, the highest in the last three years. However, the underemployment rate, which measures the part-time workers who want to work longer hours, remains high at 8.5% (at 30 November).

An improvement in wages growth is long overdue for the average Australian household, which is carrying a high level of debt and faces rising costs for non-discretionary items like healthcare and utilities. However, consumers remain cautious, with real retail sales growth averaging just 2.3% in the last couple of years. The modest pace of income growth has forced many households to reduce their savings to maintain consumption. The household saving ratio declined to 2.4% in the September quarter, the lowest saving rate since December 2007.

Despite these cost pressures for households, overall inflation remains low, with the annual rate of inflation running at 1.9% in the September quarter. Low inflation has allowed the RBA to keep the cash rate at 1.5% since August 2016. The RBA expects inflation will rise very gradually in the next few years, which means the cash rate is likely to remain stable well into 2019.

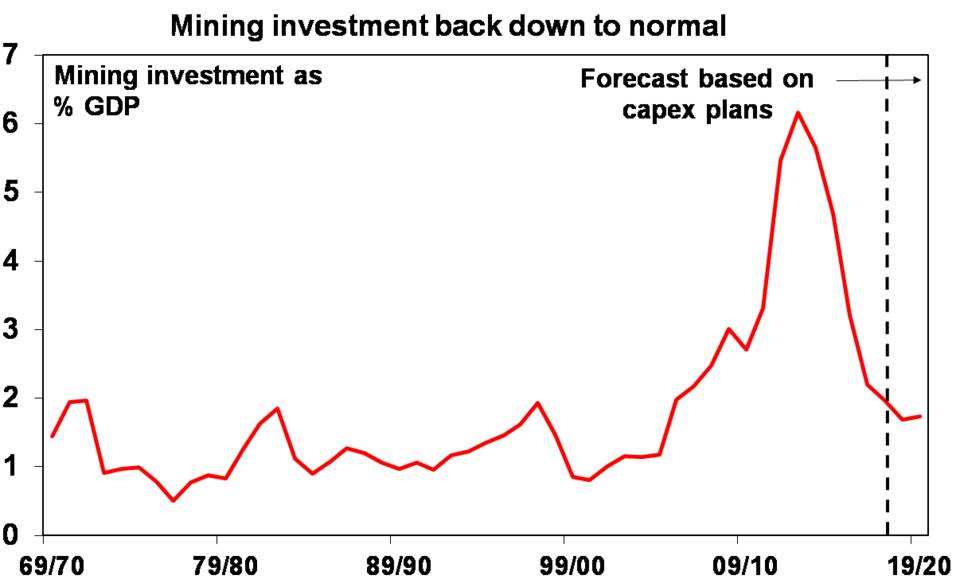

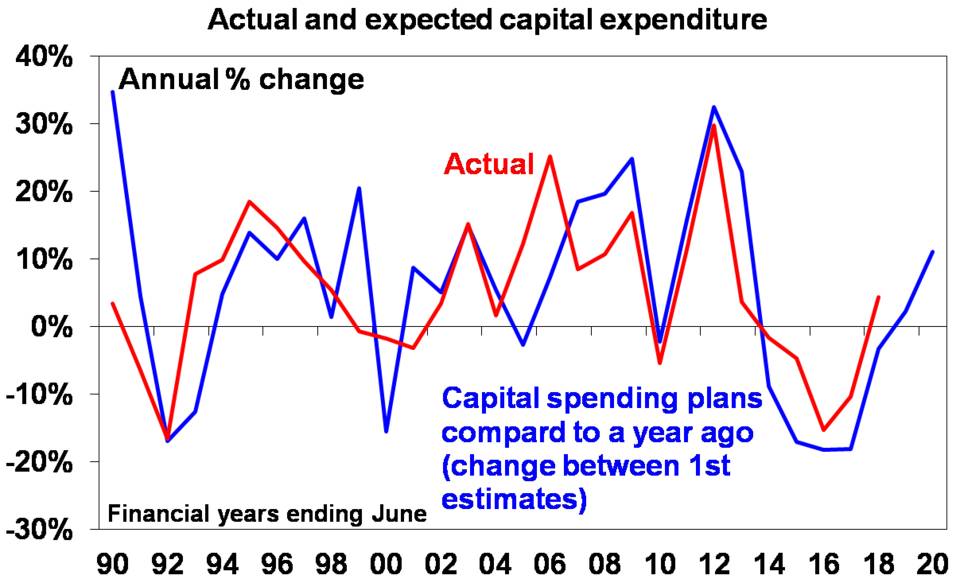

Surveys of business conditions showed a positive trend for much of 2018, although they eased towards the end of the year. Encouraging signs emerged for capital spending by the non-mining sector, with 6% growth over the year suggesting the corporate sector is finally starting to increase investment. After years of lower investment spending by the mining sector, the RBA stated in October that mining investment should grow later in 2019 as companies need to invest to sustain production. Public investment spending remained at high levels, with work continuing on a number of large infrastructure projects around the nation.

The Australian dollar weakened over the year, which benefited Australian exports. The Australian dollar fell 10% against the US dollar and was down 5.5% and 12.3% against the euro and yen respectively.

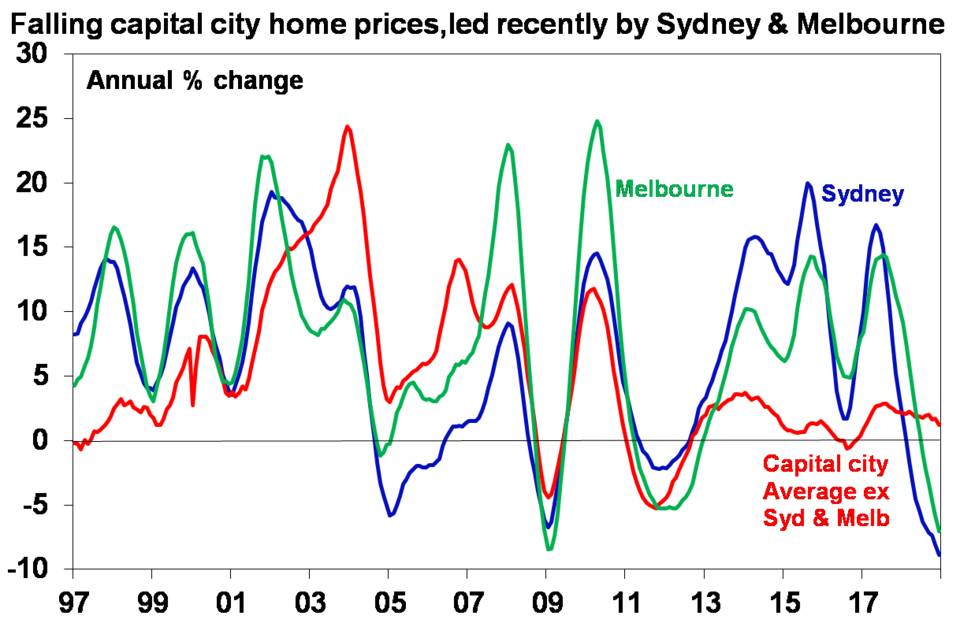

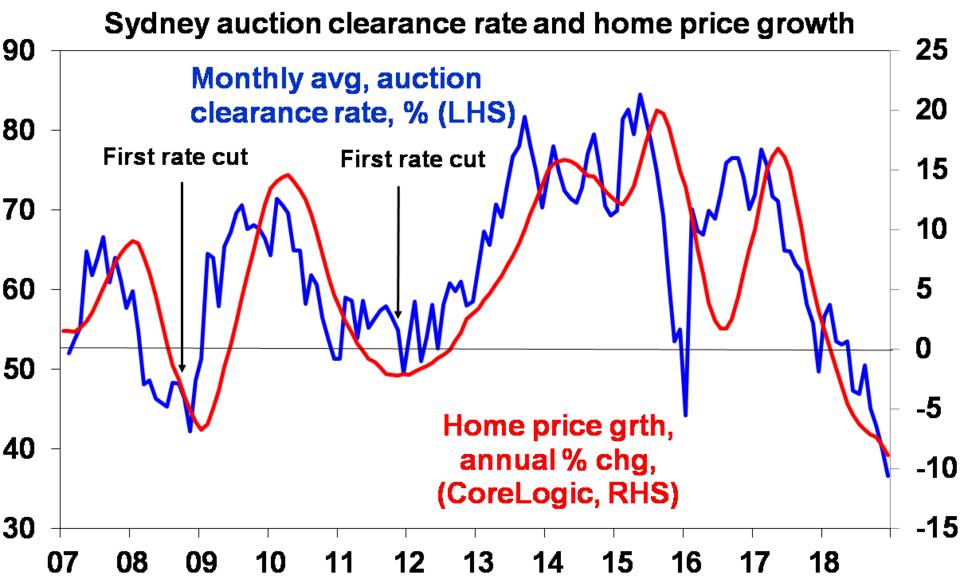

After years of strong price rises, Australian house prices fell 6% over the year, with steeper falls of 9% and 7% in the Sydney and Melbourne markets respectively. Australia’s housing market has been impacted by some banks raising mortgage interest rates and imposing more stringent lending standards, particularly for investors. Investor credit has slowed substantially and is barely growing.

Bond markets were also volatile during the year

Volatility returned to bond markets in 2018, with gradual tightening of monetary policy and withdrawal of central bank support having a wide ranging impact. With strong US economic performance continuing, the Fed kept to their forecast of four 0.25% rate rises through the year, although there are signs that they are considering a pause in the hiking cycle early in 2019. US 10-year yields rose sharply at the beginning of the year as bond prices fell. Yields eventually reached a high of 3.2% in October before falling back below 3% by year end as economic data started to weaken. Bond markets in Europe were dominated by chaotic political developments, with the ongoing Brexit debacle and a new populist Italian government worrying investors. European growth was below expectations and investors’ risk aversion meant German yields remained very low despite the closure of the ECB bond purchasing program in December.

With the US government increasing interest rates and reducing its debt, US dollar liquidity has tightened, negatively affecting bond markets this year. Investment grade and emerging markets’ bonds were the first to be affected. Although high yield bonds were fairly resilient for much of the year, they too suffered a sharp fall in their values in the last quarter as risk aversion grew. The last few years have seen rapid growth in corporate borrowing and a corresponding decline in lending standards, but until early 2018 the strong investor demand for additional yield meant the value of high credit risk bonds remained elevated. Now that even low risk bonds (eg US Treasuries) are delivering materially positive yields, investors don’t need to invest in higher credit risk bonds to get a decent yield, resulting in a shift in the supply-demand balance. In addition, increased concerns about trade wars and a potential recession in the next few years have driven a repricing of credit risk. Emerging markets endured a torrid year, with the strong US dollar putting pressure on several countries reliant on external financing.

In Australia, the RBA kept rates on hold, as reasonable economic growth was being offset by a weakening housing market. Local credit markets were largely insulated from the global sell-off.

In terms of index performance, global bonds delivered low single digit returns, with investment grade bonds slightly negative over the year in Australian dollar (hedged) terms. Local bonds outperformed global as Australian yields and spreads remained relatively stable. Bank loans significantly outperformed other high yield assets as their floating rate structure protected them from the impact of US interest rate rises, resulting in low single digit returns for the year.

In uncertain markets, a defensive portfolio stance remains justified

MLC has believed for some time that the appropriate response to the challenging investment environment is to defensively position our multi-asset portfolios − the MLC Inflation Plus, MLC Horizon and MLC Index Plus portfolios. Decisions we’ve made include:

- holding more cash than normal

- remaining highly selective about the types of bonds we invest in to limit exposure to securities that will fall in value if interest rates rise quickly

- retaining a high exposure to unhedged global shares to increase diversification

- employing innovative currency and option protection strategies to improve risk control, and

- including non-benchmark aware strategies that provide returns that are not reliant on share markets and help preserve investors’ capital in weak and volatile markets.

In the MLC Inflation Plus portfolios we’ve also employed defensive strategies such as our Defensive Australian Shares Strategy. This unique strategy has helped reduce the impact of risks specific to the Australian market, such as the high exposure to banks.

While our focus on managing risk in our multi-asset portfolios may not prevent negative returns in weak share market conditions, it should provide some insulation for investors.

How does MLC’s investment process deal with an uncertain outlook?

At MLC, we focus strongly on risk management. We believe managing risk for our investors is the sustainable way of generating returns for them – and in this unpredictable investment environment, it’s more critical than ever.

As a result, we design and manage our multi-asset portfolios to be resilient in a wide range of possible market conditions. Using our market-leading investment approach, we constantly assess how our multi-asset portfolios are likely to perform in many potential market scenarios, both good and bad. We can then adjust our portfolios to manage possible risks and take advantage of potential return opportunities.

This careful analysis means our portfolios are widely diversified, risk-aware and positioned for many market environments.