Managing your pension in volatile markets

Sinead Rafferty, Portfolio Specialist, MLC

The severe falls in global share markets in late 2018, after almost a decade of strong market returns, led many investors to ask whether it was too risky to stay invested in the share market during their retirement. If they did stay invested, should they move to a strategy with less exposure to higher risk investments, like shares?

As it turned out, markets rebounded in January, recovering most of their December losses.

It’s normal to feel anxious about your investments when markets are volatile. However, changing your investment strategy in response to market volatility can have serious consequences for your wealth in retirement. We put superannuation – specifically, account based pensions − under the microscope and look at some of the lessons we can learn from the past.

How have account based pensions performed after previous market corrections?

An account based pension is an investment that you can begin using superannuation money once you meet certain conditions. It provides a regular, tax-effective income.

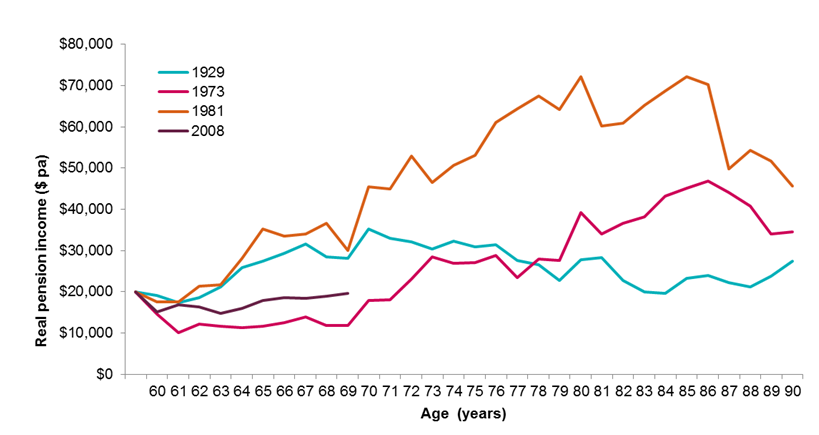

Chart 1 shows how an account based pension invested 70% in growth assets (shares and property securities) and 30% in defensive assets (fixed income and cash) would have performed if a retiree had started the pension during some key market downturns of the past. It assumes the retiree was aged 60 and had an account balance of $500,000 when they began their pension. It also assumes they drew down the minimum annual income payment each year.

Chart 1: Real annual pension incomes for selected start dates for an account based pension strategy with an asset allocation of 70% growth / 30% defensive assets.

Note: The portfolio consists of Australian shares (32%), global shares (hedged) (8%), global shares (unhedged) (24%), global property securities (6%), Australian fixed income (10%), global fixed income (10%) and cash (10%).

The sudden jumps in incomes at ages 70 and 80 are due to the rising minimum incomes investors are required to draw from account based pensions as their age increases.

Returns are based on investment market returns from 1900 to 2017 (before fees and tax). Historical returns aren’t a reliable indicator of future investment returns.

Source: Calculations by NAB Asset Management Services Limited and investment market data from Global Financial Data, Inc. and FactSet.

Chart 1 shows the annual pension payments in today’s dollars (we’ve adjusted for inflation) for an account based pension that started in four different years:

- the 2008 global financial crisis. While the initial result was particularly poor, the income levels have now recovered to pre-crisis levels.

- 1981, when the market slumped on concerns about the health of the US economy. Despite a further slump with the bursting of the dot com bubble in 2000, those who began their pension in 1981 fared well overall.

- 1973, during a period of very high inflation. While there was an initial decline, for those who maintained their investment strategy the outcome was ultimately strong as the very positive markets of the 1980s offset the 1970s.

- the start of 1929, during the Great Depression. While the pension initially performed poorly, 1932 and 1933 delivered very strong returns and the pension stream improved. Incomes suffered as a result of the share market fall in 1952, during the Korean War, but despite all these events, the outcome improved for those who remained invested.

There are important lessons in this look at history. During retirement, you should expect financial markets to deliver a wide variety of returns and at times, returns will be disappointing – as they were over the 2018 calendar year. Both positive and negative periods can continue for some time. Over time, markets generally do recover from serious downturns, but the very strong market returns that we’ve seen over the last decade are abnormally high.

If your time horizon is long enough, the higher return potential of shares usually does come through. But this can take a long time − you’ll need to be patient, and focus on how you’re progressing towards your longer-term financial goals, rather than on the frequent ups and downs of the market.

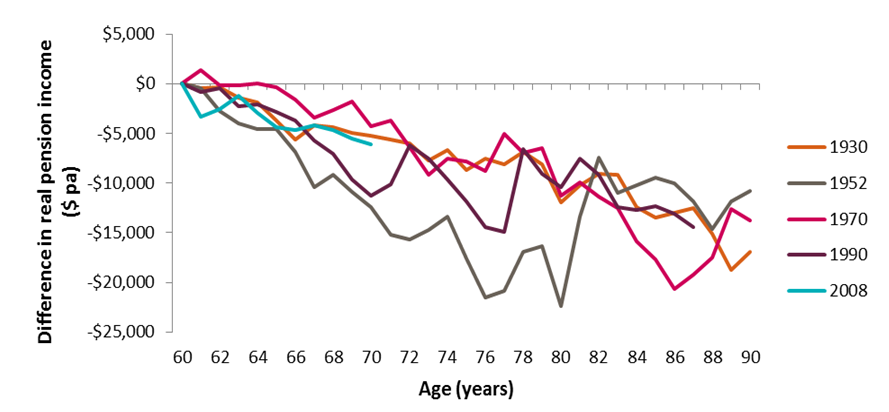

What if you switch to a more conservative strategy after a major market fall?

History teaches us another important lesson about reacting to market volatility. Assuming you’re in the right investment strategy to start with, switching to a more conservative strategy after a significant market fall probably won’t be in your best interests. Adopting this approach is likely to impact your lifestyle in retirement.

Chart 2 shows the impact on a pension income of switching from a 70% growth assets strategy to a 30% growth assets strategy after some of the worst one-year returns in history. It shows how much less you’d receive if you changed to the more conservative strategy.

Chart 2: Impact on pension payments of switching to a lower risk investment strategy after a major market fall.

Note: This chart shows the impact of moving from a portfolio with the asset allocation in Chart 1 to a portfolio consisting of Australian shares (12%), global shares (hedged) (1%), global shares (unhedged) (13%), global property securities (4%), Australian fixed income (30%), global fixed income (30%) and cash (10%).

The sudden jumps in incomes at ages 70 and 80 are due to the rising minimum incomes investors are required to draw from account based pensions as their age increases.

Historical returns aren’t a reliable indicator of future investment returns.

Source: Calculations by NAB Asset Management Services Limited and investment market data from Global Financial Data, Inc. and FactSet.

While in some cases switching to lower risk investments resulted in a short-term increase in the income the investor received, it was generally a losing strategy because it was difficult for the portfolio to recover from the significant negative returns. This could mean that an investor is drawing down more on their capital than they anticipated, so their retirement funds could run out too soon.

Conclusion

In planning a retirement strategy, it’s important to take into account both that negative market events could happen and that over time, markets generally recover from these. If you expect this, you’ll be more able to resist the temptation to sell out of the market, or move into a more conservative strategy, when a market slump occurs. By maintaining your investment strategy at these times, you’ll be well positioned to benefit when the market recovery happens.

SOURCE: https://www.mlc.com.au/personal/blog/2019/03/your-super-in-volatile-markets

Leave a Reply

Want to join the discussion?Feel free to contribute!