2020 – a list of lists regarding the macro investment outlook

Key points

- Despite ongoing bouts of volatility, 2020 is likely to provide solid returns, albeit slower than seen in 2019.

- Recession remains unlikely (it’s a bigger risk in Australia) & so too is a long deep bear market in shares.

- Watch US trade wars, the US election, the US/Iran conflict, global business conditions indicators, and monetary versus fiscal stimulus in Australia.

Introduction

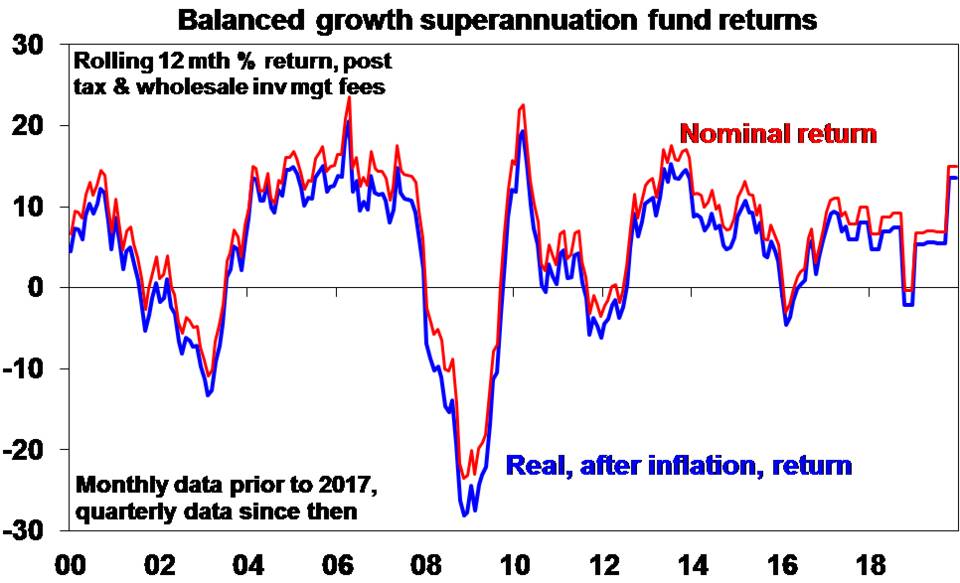

After the poor returns for investors in 2018, 2019 turned out surprisingly well with average balanced growth superannuation funds looking like they have returned around 15%.

But can it continue this year? Particularly with an intensification of the US/Iran conflict adding to global uncertainty and the drought and horrendous bushfires further weighing on the Australian economy. Here is a summary of key insights and views on the investment outlook in simple point form.

Five reasons 2019 turned out well for investors

2019 saw slowing growth and weak profits amidst an escalating US/China trade war and tensions with Iran and yet it turned out well for investors. Here are five reasons why:

- Easy money – central banks eased monetary policy in response to the growth slowdown and various threats to growth reversing the tightening seen in 2018.

- Cheap starting point for assets – after the falls of 2018 shares started 2019 cheap and they and other assets were made relatively cheaper as interest rates & bond yields fell.

- The crowd was very gloomy at the start of 2019 with much fear about the outlook – when this is the case it’s always easier for assets to rise in value.

- While geopolitical threats remained high there was some relief by year end – with the US & China reaching a Phase 1 trade deal; Iran tensions not seeing a major or lasting disruption to oil supplies; and a hard Brexit avoided for now.

- Global growth was not as bad as feared – despite a mid-year recession obsession as yield curves inverted. In fact, global growth indicators looked to be stabilising by year end.

Seven lessons from 2019

- Don’t fight the Fed, ECB, PBOC or RBA – as long as recession is avoided monetary easing is positive for investment returns from growth assets.

- The starting point matters – when assets are cheap, and the crowd is negative as they were at the start of 2019 it’s relatively easier to get good returns.

- Post GFC caution remains but can be both negative and positive – yes it periodically weighs on growth, but it is keeping economies from overheating and thereby is helping to extend the economic and investment cycle.

- Geopolitics remains a significant driver of markets and economic conditions – but it can be positive whenever there is any relief and things don’t turn out as bad as feared.

- Just because Australian housing is expensive & household debt is high does not mean house prices are going to crash.

- Stick to an investment strategy – 2019 started in gloom and had its share of distractions but investors would have done well if they just stuck to a well-diversified portfolio.

- Remember that while shares can be volatile and unlisted assets also come with risks, the income stream from a well-diversified mix of such assets can be relatively stable and higher than the income from bank deposits.

Five big picture themes for 2020

- A pause in the trade war, but geopolitical risk to remain high. President Trump is likely to want to keep the US/China trade war on the backburner but it could still flare up again and other issues include the escalation seen so far this year in the Iran conflict, a return to worries about a “hard Brexit” at year end if UK/EU free trade talks don’t go well and the US election if a hard left Democrat candidate gets up.

- Global growth to stabilise & turn up thanks to policy stimulus with business surveys recently showing stabilisation.

- Continuing low inflation and low interest rates. Growth won’t be strong enough to push underlying inflation up much and some central banks will still be easing (including the RBA).

- The US dollar is expected to peak and head down as global uncertainty declines a bit and non-US growth picks up.

- Australian growth is expected to remain weak given the housing construction downturn, weak consumer spending and the drought with bushfires not helping.

Key views on markets for 2020

Improving global growth & still easy monetary conditions should drive reasonable investment returns this year but they are likely to be more modest than the double-digit gains of 2019 as the starting point of higher valuations for shares & geopolitical risks are likely to constrain gains and create some volatility:

- Global shares are expected to see total returns around 9.5% in 2020 helped by better growth and easy monetary policy.

- Cyclical, non-US and emerging market shares are likely to outperform, if the US dollar declines as we expect.

- Australian shares are likely to do okay this year but with total returns also constrained to around 9% given sub-par economic & profit growth.

- Low starting point yields and a slight rise in yields through the year are likely to result in low returns from bonds.

- Unlisted commercial property and infrastructure are likely to continue benefitting from the search for yield but the decline in retail property values will still weigh on property returns.

- National capital city house prices are expected to see continued strong gains into early 2020. However, poor affordability, the weak economy and still tight lending standards are expected to see the pace of gains slow leaving property prices up 10% for the year as a whole.

- Cash & bank deposits are likely to provide very poor returns, with the RBA expected to cut the cash rate to 0.25%.

- The $A is likely to fall to $US0.65 as the RBA eases further, then drift up as global growth improves to end little changed.

Seven things to watch

- The US trade wars – we are assuming the Phase 1 trade deal de-escalates the trade war, but Trump is Trump and often can’t help but throw grenades.

- US politics: the Senate is unlikely to remove Trump from office if the House votes to impeach and another shutdown is also unlikely but both could cause volatility as could the US election if a hard-left Democrat gets up (albeit unlikely).

- The US/Iran conflict – which could escalate further with Iran unlikely to negotiate and Trump wanting to sound tough, potentially disrupting oil supplies.

- A hard Brexit looks like being avoided but watch UK/EU free trade negotiations through the year.

- Global growth indicators (PMIs).

- Chinese growth – a continued slowing in China would be a major concern for global growth.

- Monetary v fiscal stimulus in Australia – significant fiscal stimulus could head off further RBA easing.

Four reasons global growth is likely to improve a bit

- Global monetary conditions have eased significantly over the last year. China has also seen significant fiscal stimulus.

- The stabilisation seen in business conditions PMIs in recent months suggests monetary easing is getting some traction.

- We still have not seen the excesses – massive debt growth, overinvestment, capacity constraints or excessive inflation – that normally precede recessions.

- The de-escalation of the US/China trade war should help reduce a drag on business confidence (at least for a while).

Five reasons Australia is likely to avoid a recession

The bushfires are estimated to knock around 0.4% mainly from March quarter GDP mainly due to the impact on agriculture, tourism and consumer confidence and spending. Coming at a time when Australian growth is already weak it risks knocking March quarter growth to near zero or below. However, while the risk of recession has increased, it remains unlikely:

- Infrastructure spending is strong.

- Mining investment is starting to rise again.

- The bushfires will be followed by a boost to spending from the June quarter as rebuilding kicks in.

- Already weak growth, made worse by the bushfires in the short term will likely force further fiscal stimulus.

- The $A is likely to remain weak providing a boost to growth.

Three reasons why the RBA will cut rates this year

- Growth is likely to disappoint RBA expectations for 2.8% growth this year.

- This will keep underemployment high, wages growth weak and inflation lower for longer.

- Fiscal stimulus is unlikely to come early enough.

We expect the RBA to cut the cash rate to 0.5% in February & to 0.25% in March, with quantitative easing likely from mid-year.

Three reasons why a deep bear market is unlikely

Shares are vulnerable to a correction after the strong gains seen over the last year, but a deep bear market (where shares fall 20% and a year after are a lot lower again) is unlikely:

- Global recession remains unlikely. Most deep bear markets are associated with recession.

- Measures of investor sentiment suggest investors are cautious, which is positive from a contrarian perspective.

- The liquidity backdrop for shares is still positive. For example, bank term deposit rates in Australia are around 1.3% (and likely to fall) compared to a grossed-up dividend yield of around 5.7% making shares relatively attractive.

Nine things investors should remember

- Make the most of the power of compound interest. Saving regularly in growth assets can grow wealth substantially over long periods. Using the “rule of 72”, it will take 48 years to double an asset’s value if it returns 1.5% pa (ie 72/1.5) but only 9 years if the asset returns 8% pa.

- Don’t get thrown off by the cycle. Falls in asset markets can throw investors out of a well thought out strategy at the wrong time – as some were at the end of 2018.

- Invest for the long term. Given the difficulty in getting short term market moves right, for most it’s best to get a long-term plan that suits your wealth, age & risk tolerance & stick to it.

- Diversify. Don’t put all your eggs in one basket.

- Turn down the noise. Increasing social media and the competition for your eyes and ears is creating a lot of noise around investing that is really just a distraction.

- Buy low, sell high. The cheaper you buy an asset, the higher its prospective return will likely be and vice versa.

- Beware the crowd at extremes. Don’t get sucked into the euphoria or doom and gloom around an asset.

- Focus on investments that you understand and that offer sustainable cash flow. If it looks dodgy, hard to understand or has to be based on odd valuation measures or lots of debt to stack up then it’s best to stay away.

- Accept that it’s a low nominal return world – when inflation is 1.5%, a 15% superannuation return is very pretty good (and not sustainable at that rate).

Leave a Reply

Want to join the discussion?Feel free to contribute!