How to diversify when investing in bonds no longer works

Bonds have traditionally helped diversify the risk of shares because bond and share prices tend to move in opposite directions. But what if both bond and share prices fall at the same time, so that this diversification no longer works? MLC provides some insights about how they manage this challenge in their portfolios.

Why does diversification matter?

In an investment portfolio, diversification, or investing across many types of assets, is essential. The prices of different assets tend to rise and fall at different times, so investing in a mix of assets means risk is spread out and the portfolio is less exposed to the ups and downs of returns of individual assets.

Bonds, the traditional diversifier, aren’t working

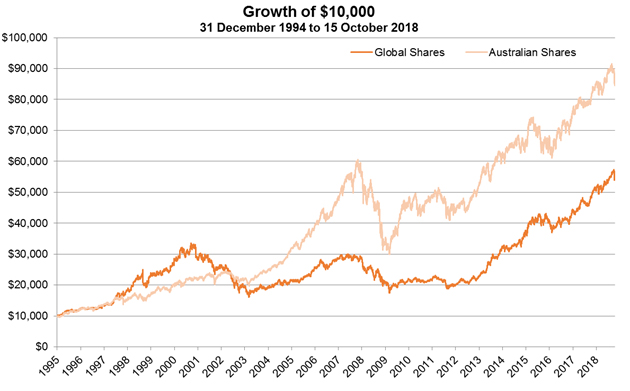

Over the long term, the highest returns tend to come from shares. Shares do particularly well when economic growth is strong. If economic growth and therefore company earnings are lower than expected, share prices tend to decline. Bonds tend to do well when the economy is weak, so when share prices fall, they should reduce the negative impact on a portfolio.

Bonds have traditionally been used to diversify the risk of investing in shares because bond and share prices tend to move in opposite directions. But what if both bond and share prices fall at the same time, so that this diversification doesn’t work? In today’s market, there’s a much higher risk of this than usual. That’s because bond yields are unusually low, which means bond prices are unusually high (bond yields and prices move in opposite directions). Any asset which is expensive is vulnerable to a fall – for example, bond prices are vulnerable to higher than expected inflation and interest rates.

But why are bond yields so low, and bond prices so high?

After the global financial crisis struck, central banks took extraordinary steps to support the financial system. This included drastically lowering interest rates and buying bonds to increase liquidity. This reduced the supply of bonds, which raised their prices and lowered their yields. Investors hunting for returns were forced into more risky assets, making everything expensive at the same time.

This has been great for investors, who have received strong returns. But it also means that almost all assets are potentially vulnerable to rising interest rates as central banks move back to more normal policies. The normalisation process has begun and this is a key reason for more volatility in both bond and share markets. Since the prices of bonds and shares may fall together, bonds may not play their normal diversifying role.

Because of this risk and unusually low bond yields, we’ve had very little or no exposure to conventional bonds in our MLC Inflation Plus portfolios, and have been significantly underweight in the MLC Horizon and MLC Index Plus portfolios, for some time. This means it’s been important to find other ways of diversifying share market risk. A key strategy has been using foreign currency exposure.

How can foreign currency exposure help solve the diversification problem?

Australia’s economy relies heavily on exporting natural resources, such as iron ore. This means our dollar tends to rise when the global economy is growing strongly. Global share markets also tend to perform well in these circumstances.

When global share markets weaken due to concerns about economic growth, the Australian dollar tends to decline. So reducing our exposure to the Australian dollar, by holding more of other currencies, can help to insulate our portfolios against losses when global share markets fall.

In recent years we’ve increased the exposure to foreign currencies such as the US dollar in our portfolios, allowing us to benefit from the returns of global share markets while helping to manage the risk of those markets falling. This diversification strategy has been very successful, both for making returns and reducing risk. This is particularly so for the MLC Inflation Plus portfolios, where we’ve used derivatives to manage the exposure at zero cost. By using derivatives, we’ve benefited more from rising share markets, while helping manage their risks.

Our dollar has fallen against the US dollar over the last couple of years. This makes foreign currency exposure less powerful as a diversifier, so we’ve reduced our exposure over time. However, the investment environment has very few diversification opportunities and exposure to foreign currency – including the yen, the British pound and the euro – is still a helpful strategy for controlling risk in our portfolios.

In unpredictable and constantly changing markets, we’ll continue to look for new ways to help provide returns and manage risk for our investors.

SOURCE: https://www.mlc.com.au/personal/blog/2019/01/how_to_diversifywhe